Understanding the average variable cost (AVC) formula is crucial for any business aiming to optimize its production processes. The AVC formula is fundamental in determining the cost of production that varies directly with the level of output. It’s a critical metric for making informed decisions about pricing, cost control, and operational efficiency.

Practically speaking, knowing the AVC allows a business to pinpoint the minimum price it can charge to cover its variable costs, ensuring profitability. Additionally, AVC can highlight inefficiencies in production, guiding businesses to streamline operations and reduce waste.

Key Insights

- Primary insight with practical relevance: AVC is a vital metric for understanding the short-term cost dynamics within a production process.

- Technical consideration with clear application: In production planning, AVC helps identify breakeven points where total revenues match total variable costs.

- Actionable recommendation: Regularly calculating AVC and comparing it with the price at which products are sold can provide significant insights for cost management and pricing strategies.

The Significance of Average Variable Cost

The average variable cost formula is pivotal for cost management, especially in a business landscape where costs can fluctuate significantly based on production levels. AVC includes all costs that change with the level of output, such as raw materials, direct labor, and some utilities. Unlike fixed costs, these costs do not remain constant and instead vary with the quantity of goods produced.Understanding the AVC provides businesses with a granular view of their production expenses, enabling more precise control over spending and more accurate forecasting. For instance, if a business notices that its AVC is rising faster than its output, it might indicate a need to renegotiate with suppliers for better rates or to invest in more efficient production methods.

Calculating Average Variable Cost

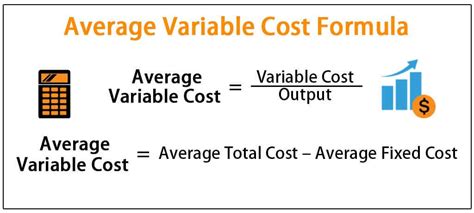

To calculate AVC, one divides total variable costs by the number of units produced. The formula can be expressed as: AVC = Total Variable Costs / Quantity of Units Produced.For example, consider a manufacturing company producing 1,000 units of a product. The total variable costs incurred for this production amount to 10,000. By applying the AVC formula, we get: AVC = 10,000 / 1,000 units = 10 per unit. This calculation clearly shows that each unit costs 10 in variable expenses. By analyzing this data, the company can identify whether its variable costs are under control and if they can negotiate better rates with suppliers.

Understanding and accurately calculating AVC can help businesses adjust their production strategies, ensuring they maintain profitability without overextending on variable costs.

How does AVC differ from total variable cost?

While total variable cost (TVC) is the sum of all costs that change with production levels, AVC specifically measures the cost per unit of production. Understanding AVC provides a clearer picture of per-unit variable costs, which is crucial for pricing decisions and operational efficiency.

What is the relationship between AVC and pricing strategies?

The relationship between AVC and pricing is significant for ensuring profitability. Businesses should aim to price their products above the AVC to cover variable costs and ideally above the AVC plus a margin to cover fixed costs and generate profit. Understanding this relationship helps in setting competitive yet profitable prices.

In summary, the average variable cost formula is a cornerstone in operational and financial analysis, providing a clear, quantifiable way to understand and manage production costs. Through accurate AVC calculations and strategic implementation, businesses can achieve greater control over their cost structures, leading to improved profitability and operational efficiency.