Understanding the key determinants of demand is crucial for businesses striving to optimize their market strategy and maximize profitability. This article delves into the intricate elements that influence consumer purchasing decisions, offering actionable insights and practical examples.

Context and Hook

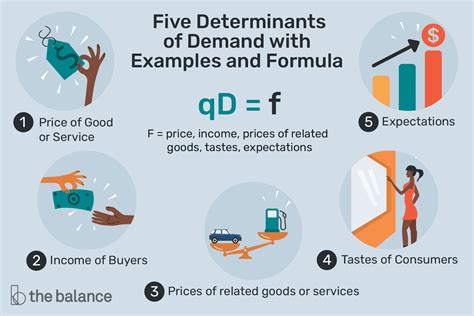

Demand, at its core, represents the quantity of a product or service that consumers are willing and able to purchase at various price points over a given period. Recognizing what drives demand isn’t just an academic exercise; it’s a vital skill for business leaders aiming to craft informed, strategic decisions. This article uncovers the fundamental determinants of demand and offers a practical framework for businesses to leverage these insights.

Key Insights

- Consumer income levels significantly impact demand, with higher incomes generally leading to higher demand for most goods.

- Substitute and complementary goods play a pivotal role in demand fluctuations, influencing consumer choices.

- Implementing market segmentation can enhance demand forecasting and help target specific consumer groups effectively.

Income Levels as a Primary Driver

Consumer income directly correlates with demand, often described as the income elasticity of demand. A positive income elasticity implies that demand increases with higher income levels. For example, luxury brands typically experience increased demand during economic booms when consumer wealth rises. Conversely, during recessions, demand for such goods often drops due to reduced disposable income. For businesses, understanding this relationship can inform pricing strategies and marketing campaigns that resonate with consumers’ financial capabilities.

The Role of Substitutes and Complements

Substitute and complementary goods significantly affect demand dynamics. Substitute goods are those that can replace each other, such as tea and coffee or smartphones and tablets. When the price of one good increases, the demand for its substitute often rises. For instance, if the price of gasoline surges, consumers may switch to public transportation or hybrid vehicles. On the other hand, complementary goods are those that are used together, such as printers and ink cartridges. For businesses, understanding these relationships can lead to strategic partnerships or bundled offerings that enhance overall demand.

What role do trends and seasonality play in demand?

Trends and seasonality significantly influence demand. Seasonal products, like winter coats or holiday decorations, have predictable demand patterns. Trends, whether driven by social media, celebrity endorsements, or innovative technology, can create sudden shifts in demand. Businesses that adapt their inventory and marketing strategies to align with these trends can capitalize on rising demand effectively.

How do consumer preferences impact demand?

Consumer preferences, shaped by cultural, social, and personal factors, play a substantial role in demand. For instance, health-conscious consumers may drive demand for organic food products. Companies must stay attuned to these shifts, innovating and adapting their offerings to meet evolving consumer tastes and expectations.

To sum up, understanding the key determinants of demand, including income levels, substitute and complementary goods, trends, and consumer preferences, provides a comprehensive framework for businesses to anticipate and respond to market dynamics. Armed with these insights, businesses can make more informed decisions that drive growth and enhance their competitive edge.