I’ll create a blog post about maximizing TSP (Thrift Savings Plan) contributions for Department of Defense (DoD) employees. I’ll follow the specified guidelines carefully:

Navigating the world of retirement savings can be challenging, especially for Department of Defense (DoD) employees looking to max out TSP contributions. The Thrift Savings Plan offers a powerful opportunity for federal workers to build a robust financial future, providing a tax-advantaged path to long-term wealth accumulation.

Understanding TSP Contribution Limits

For DoD employees, maximizing TSP contributions requires a strategic approach. In 2026, the annual contribution limits provide significant opportunities for federal workers to save for retirement. The Internal Revenue Service (IRS) sets specific guidelines that allow participants to:

- Contribute up to $23,500 in elective deferrals for the year

- Take advantage of catch-up contributions for those 50 and older

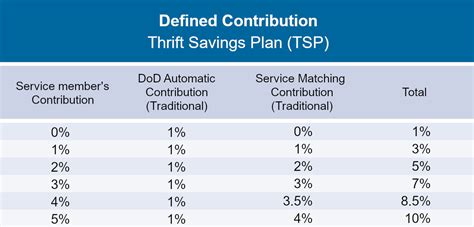

- Potentially add additional funds through agency matching

Strategies to Maximize Your TSP Contributions

Implementing a comprehensive strategy can help DoD employees optimize their retirement savings. Consider the following approaches:

- Front-load Your Contributions

Distribute your contributions strategically throughout the year to ensure you're maximizing your potential savings. This approach helps you take full advantage of the annual contribution limits.

- Utilize Catch-up Contributions

If you're 50 or older, you can make additional catch-up contributions, increasing your total potential savings beyond the standard limit.

- Leverage Matching Contributions

DoD employees should take full advantage of agency matching, which can significantly boost your retirement savings at no additional cost to you.

Tax Advantages of Maximizing TSP

The tax benefits of maxing out your TSP contributions are substantial. Depending on the type of TSP account you choose:

| TSP Type | Tax Benefit |

|---|---|

| Traditional TSP | Contributions reduce current taxable income |

| Roth TSP | Tax-free withdrawals in retirement |

💡 Note: Carefully consider your current and future tax situation when choosing between Traditional and Roth TSP options.

Common Challenges in Maximizing Contributions

Many DoD employees struggle to max out their TSP due to various financial constraints. Some practical solutions include:

- Creating a detailed budget

- Gradually increasing contribution percentages

- Reducing unnecessary expenses

Reaching your maximum TSP contribution requires discipline, planning, and a commitment to your financial future. By understanding the nuances of the Thrift Savings Plan and implementing strategic saving techniques, DoD employees can build a robust retirement nest egg.

What is the current TSP contribution limit?

+

As of 2026, the annual contribution limit is $23,500, with additional catch-up contributions available for those 50 and older.

Can I contribute to both Traditional and Roth TSP?

+

Yes, you can split your contributions between Traditional and Roth TSP, but the total cannot exceed the annual contribution limit.

What happens if I exceed the TSP contribution limit?

+

Exceeding the contribution limit may result in tax penalties and required corrective distributions from your account.