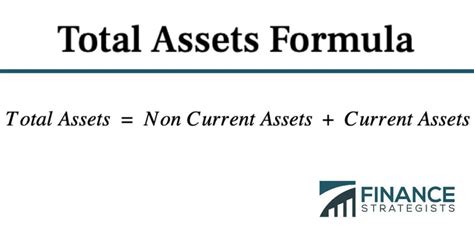

Calculating total assets is a crucial task in financial management whether you’re managing your personal finances or handling a business’s financial statements. Understanding how to do it accurately can give you a clear picture of your financial health. This guide will walk you through everything you need to know, with step-by-step guidance, practical solutions, and actionable tips to help you master this fundamental financial skill.

Problem-Solution Opening Addressing User Needs

Calculating total assets might seem like a daunting task, especially if you’re new to financial management. The numbers involved, the different types of assets, and the complexity of financial statements can make it overwhelming. However, this calculation is vital for assessing both personal and business financial health. By understanding and calculating total assets accurately, you can make informed decisions about spending, investing, and planning for the future. This guide will break down the process into easy-to-follow steps, provide real-world examples, and equip you with tips and best practices to ensure you get it right every time. Let’s dive into the clear, practical steps to calculate total assets today!

Quick Reference

Quick Reference

- Immediate action item: Identify all your assets including cash, investments, property, and other valuable possessions.

- Essential tip: Use a spreadsheet to organize your assets. List each asset in a column and note their value in the adjacent column for easy calculation.

- Common mistake to avoid: Overlooking non-liquid assets like property or investments. Make sure you account for everything to get an accurate total.

How to Calculate Total Assets for Individuals

Calculating total assets for individuals is relatively straightforward once you understand the components. Let’s break it down step-by-step.

Step 1: List All Your Assets

Begin by listing everything you own that has value. This includes:

- Cash and checking accounts

- Savings accounts and certificates of deposit (CDs)

- Investments like stocks, bonds, and mutual funds

- Real estate properties (primary home, vacation homes, etc.)

- Precious metals (gold, silver)

- Collectibles (artwork, vintage cars)

- Personal property like furniture and vehicles

Step 2: Determine the Market Value of Each Asset

Next, determine the current market value of each asset. For most liquid assets, like cash and investments, this will be straightforward. For non-liquid assets, you may need to consult an appraiser or check recent sales of similar items.

Step 3: Sum Up the Values

Once you have the market value for each asset, add them all together to get your total assets. For example, if your cash is valued at 5,000, your stocks at 30,000, and your home at 300,000, your total assets would be: <strong>5,000 + 30,000 + 300,000 = $335,000.

Step 4: Use a Spreadsheet for Organization

To make the process easier, use a spreadsheet to organize your assets. Here’s how:

- Create columns for asset type, market value, and total.

- List each asset in the asset type column.

- Input the market value in the market value column.

- Use a formula to automatically calculate the total.

Step 5: Verify and Update Regularly

Financial values change over time, so it’s essential to verify and update your total assets regularly. At least once a year, review and update the values of your assets to ensure accuracy.

Tips and Best Practices

- Use online tools or financial apps to get up-to-date market values.

- Keep records of all transactions related to your assets.

- Consider professional help if your assets are particularly complex or valuable.

How to Calculate Total Assets for Businesses

For businesses, calculating total assets involves more intricate steps as companies usually deal with a wider range of assets. Here’s how you can approach it.

Step 1: Identify Current and Non-Current Assets

First, categorize your assets into current and non-current (long-term) assets. Current assets include:

- Cash and cash equivalents

- Accounts receivable

- Inventory

- Prepaid expenses

- Property, plant, and equipment (PP&E)

- Intangible assets like patents and trademarks

- Long-term investments

- Current Assets: Use the most recent accounting records.

- Non-Current Assets: Check your balance sheet where these values are recorded.

- Maintain detailed records for all asset-related transactions.

- Use depreciation schedules to update the book value of non-current assets.

- Consult with a financial advisor or accountant for complex asset calculations.

- List all your investments including stocks, bonds, mutual funds, etc.

- Determine the current market value of each investment. You can use financial websites or apps to get real-time prices.

- For any investments held in retirement accounts, use the most recent account statements to get the accurate value.

- Add up all the values of your investments to get the total value of this category.

- Include this total in your overall total assets calculation.

Step 2: Determine the Market Value or Book Value of Each Asset

For current assets, market value is generally equal to book value. For non-current assets, you might need to refer to financial statements where these are recorded at their book value. Here’s how you can determine these values:

Step 3: Add Up the Values of All Assets

Once you have the values for all your assets, add them together to get your total assets. For example, if your current assets are valued at 500,000 and your non-current assets at 2,000,000, your total assets would be: 500,000 + 2,000,000 = $2,500,000.

Step 4: Use Accounting Software for Organization

To manage large sets of data, use accounting software like QuickBooks, Xero, or Sage. These tools help you organize, track, and calculate asset values efficiently.

Step 5: Regular Review and Updates

It’s crucial to review and update asset values regularly to ensure accuracy. Schedule regular audits and make sure all changes are recorded properly in your accounting system.

Tips and Best Practices

Practical FAQ

Common user question about practical application

One common question is how to accurately account for investments when calculating total assets. To address this, here’s what you need to do:

This detailed guide has provided you with a comprehensive, step-by-step approach to calculating total assets whether you’re managing personal finances or overseeing a business’s financial health. Remember, accurate asset calculations are foundational to effective financial planning. Regularly update your records and use the right tools to keep your financial picture clear and actionable. Follow these practical steps and tips to make sure you never miss an asset and always have a solid understanding of your financial position. Happy calculating!