In the complex world of commercial and personal real estate, the differentiation between leasing and financing is often blurred by lay understanding and even some professional misunderstandings. At its core, both strategies serve as pivotal tools for acquiring property, yet they fundamentally differ in intent, structure, risk distribution, and long-term implications. As an expert in financial and leasing arrangements with over two decades of hands-on experience in real estate law, economic analysis, and asset management, I aim to unravel these distinctions to provide clarity. Whether you're a seasoned investor, a business owner contemplating expansion, or a novice navigating the property acquisition landscape, grasping the nuanced differences between lease agreements and financing options will empower more strategic decision-making.

Key Points

- Understanding lease versus finance involves clarifying the ownership, payment structure, and contractual obligations.

- Lease agreements focus on usage rights, often with tax and accounting nuances that influence decision-making.

- Financial arrangements, particularly loans, involve ownership transfer and debt obligations, affecting balance sheets and cash flows.

- Long-term implications of each approach influence investment strategies, liquidity, and asset control.

- Context-specific insights help determine the optimal approach based on organizational goals and financial health.

Fundamental Differences Between Leasing and Financing

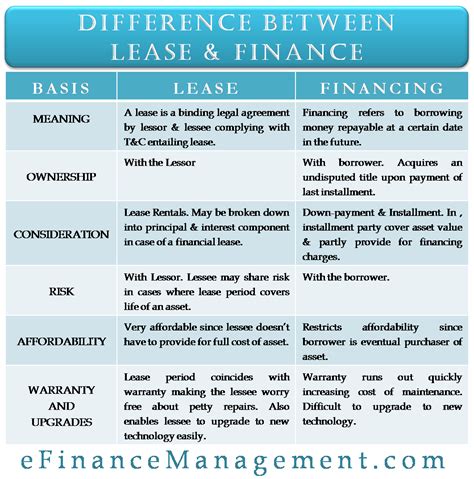

The primary distinction between leasing and financing lies in ownership rights and the purpose of the contractual relationship. A lease grants the lessee the right to use an asset—be it property, equipment, or vehicle—for a specified period in exchange for periodic payments. By contrast, financing—often through loans or mortgages—enables the borrower to acquire ownership of an asset outright, with the obligation to repay principal and interest over time. These differences are reflected in their structural frameworks, accounting treatments, tax implications, and strategic uses.

Ownership and Control: Who Holds the Title?

In a typical leasing scenario, title or ownership remains with the lessor—often a property owner or financial institution—while the lessee gains the right to use the asset within the lease term. This arrangement primarily addresses usage and occupancy without transferring ownership rights. Conversely, financing transfers ownership to the borrower, who assumes control, rights, and responsibilities associated with the property’s maintenance, tax payments, and eventual disposition. This distinction influences decision-making in strategic asset management, particularly concerning depreciation, tax benefits, and potential residual value.

| Relevant Category | Substantive Data |

|---|---|

| Ownership Transfer | In leasing: No; in financing: Yes, at the conclusion of the payment schedule or through a purchase clause. |

| Liability and Risk | Leasing: Risk remains with lessor; financing: Risk shifts to borrower, including depreciation and market value fluctuations. |

| Tax Treatment | Leases often classified as operating expenses; financed assets may qualify for depreciation deductions and interest expense. |

| Balance Sheet Impact | Leases: Often off-balance-sheet (for operating leases before recent standards), whereas financed assets appear as liabilities and fixed assets. |

Structural Frameworks and Contractual Nuances

The structural architecture of leasing agreements is designed to be flexible, with a focus on mitigating initial capital expenditure and providing operational convenience. Operating leases, for example, typically have shorter durations, minimal maintenance obligations, and no transfer of risk related to ownership. Capital leases (or finance leases), on the other hand, closely resemble financing arrangements, often involving bargain purchase options, longer durations, and significant residual value considerations.

Operational vs. Financial Leases: Strategic Implications

The delineation between operational and financial leases facilitates tailored financial strategies for different asset types and organizational needs. Operating leases are often favored for equipment or assets with rapid obsolescence, minimizing on-balance-sheet liabilities and enabling easy upgrades. Significant finance leases, however, are suitable when an organization aims to eventually own the asset and fully amortize the associated costs over its useful life. This strategic choice impacts financial ratios, tax planning, and liquidity management.

| Relevant Category | Substantive Data |

|---|---|

| Lease Duration | Typically less than the asset’s useful life for operating leases; equivalent or longer for finance leases. |

| Payment Structure | Periodic rent or amortized payments; often includes residual or purchase options in finance leases. |

| Maintenance Responsibilities | Generally with the lessee in finance leases; less so in operating leases unless specified. |

| Accounting Standards | Recent standards (e.g., IFRS 16) require many leases to be recognized on the balance sheet, affecting strategic reporting. |

Tax and Accounting Impacts: Strategic Considerations

The tax treatment of lease and finance arrangements offers compelling incentives and complexities. Lease payments are typically deductible as operating expenses, processing as a reduction in taxable income (subject to jurisdictional limitations). Conversely, financed assets enable companies to leverage depreciation deductions and deduct interest expenses, which can be substantial depending on loan terms and tax laws.

Impact of Recent Accounting Standards

Introducing standards like IFRS 16 and ASC 842 has standardized lease reporting, compelling organizations to recognize nearly all leases on their balance sheets. This shift impacts key financial ratios such as debt-to-equity and EBITDA, altering perceptions of leverage and profitability. Developers and asset managers must now carefully evaluate lease structures to optimize tax benefits without compromising financial transparency.

| Relevant Category | Substantive Data |

|---|---|

| Tax Deductibility | Lease payments as operating expenses; depreciation + interest in financed assets. |

| Impact on Financial Ratios | Leases previously off-balance-sheet now recognized, affecting ratios like debt-to-assets. |

| Strategic Tax Planning | Leasing can preserve liquidity, while financing offers tax shields through depreciation. |

Long-Term Strategic Effects and Risk Management

From a broader perspective, the decision to lease or finance carries profound implications for an organization’s long-term strategic posture. Leasing provides operational flexibility, lower upfront investment, and mitigates obsolescence risk, but potentially sacrifices ownership benefits. Financing facilitates asset accumulation, equity building, and residual value capture, yet introduces higher debt levels and market-dependent valuation risks.

Risk Distribution: Who Bears the Burden?

In leasing arrangements, the lessor assumes the risk of asset depreciation and obsolescence, providing a buffer for the lessee. Meanwhile, financing transfers some risk to the borrower but exposes them to residual market risk and fluctuating interest rates, especially in variable-rate loans. Risk appetite influences choice: organizations seeking control and ownership tend to favor financing, while those prioritizing operational agility lean toward leasing.

| Relevant Category | Substantive Data |

|---|---|

| Obsolescence Risk | With the lessor in lease arrangements; with the borrower in financed purchases. |

| Market Value Fluctuations | Significant for financed assets, affecting residual values and collateral. |

| Liquidity Impact | Lease payments are predictable expenses; financing impacts cash flows and debt covenants. |

Practical Applications and Decision-Making Frameworks

What factors guide the choice between leasing and financing in practical settings? Generally, decision-makers evaluate asset usage needs, tax considerations, financial health, and market conditions. For example, rapidly evolving technology equipment often benefits from leasing structures that minimize obsolescence risk. Conversely, large property purchases with long-term value potential are better suited for financing, especially if favorable interest rates are available.

Decision Trees and Financial Modeling

Employing sophisticated financial modeling tools, including net present value (NPV), internal rate of return (IRR), and scenario analysis, allows organizations to quantify the long-term impacts of each approach. These models incorporate variables such as interest rate fluctuations, tax effects, residual value, and inflation — ensuring well-informed strategic choices rooted in rigorous analysis.

| Relevant Category | Substantive Data |

|---|---|

| Modeling Techniques | NPV, IRR, sensitivity analysis incorporating variables like interest rate, tax effects, residual value. |

| Strategic Fit | Aligning asset acquisition strategies with organizational lifecycle and growth projections. |

Future Trends and Evolving Practices in Lease and Finance Strategies

The dynamic landscape of real estate and equipment acquisition continues to evolve, driven by macroeconomic shifts, technological innovations, and changing regulatory standards. The rise of smart contracts and blockchain-based leasing platforms promises increased transparency and efficiency, potentially transforming traditional lease agreements into programmable, automated contracts. Simultaneously, low-interest rate environments worldwide have made financing more attractive, fueling capital investments in key sectors.

Digital Transformation and Smart Contracts

Early adopters are exploring smart contracts for automating lease payments, compliance, and renewal clauses, leading to reduced administrative burden and increased trust. These technology trends are expected to catalyze a shift toward more flexible, data-driven asset management models that blur the traditional boundaries of leasing and financing.

| Relevant Category | Substantive Data |

|---|---|

| Innovation Impact | Automation, increased transparency, reduced transaction costs in lease agreements via blockchain and smart contracts. |

| Interest Rate Environment | Historically low rates globally support financing; volatility can influence the decision balance. |

| Regulatory Changes | Emerging standards impact lease classification and disclosure, affecting strategic planning. |

Final Perspectives: Aligning Strategy with Organizational Goals

Ultimately, discerning the nuanced differences between leasing and financing hinges on aligning each approach with overarching organizational objectives. Flexibility, risk appetite, tax optimization, ownership aspirations, and market outlooks are all facets of a comprehensive strategic framework. The insights shared here aim to foster informed decision-making, ensuring that asset acquisition strategies support sustainable growth while managing inherent risks effectively.

How does lease accounting impact financial statements?

+Modern lease accounting standards like IFRS 16 and ASC 842 require organizations to recognize nearly all leases on balance sheets, with right-of-use assets and corresponding liabilities. This increases transparency but also affects key ratios such as debt-to-equity and EBITDA, potentially impacting investor perception and borrowing capacity.

What criteria determine whether to lease or finance a property?

+Decision criteria include asset usage frequency, expected residual value, cash flow considerations, tax implications, technological obsolescence risk, and strategic control desires. High-usage, long-term assets typically benefit from financing, while shorter-term, flexible assets lean toward leasing.

Are there industries where leasing is predominantly preferred over financing?

+Yes, sectors such as technology, transportation, and retail often prefer leasing due to rapid obsolescence, minimal upfront investment, and operational flexibility. This approach allows them to adapt swiftly to market changes without heavy capital commitments.

How might future technological developments influence lease vs. finance decisions?

+Emerging technologies like blockchain, IoT-enabled asset management, and smart contracts may streamline lease administration, reduce costs, and introduce new contractual models. These innovations could favor more dynamic, automated leasing structures, shifting traditional paradigms.